You have /5 articles left.

Sign up for a free account or log in.

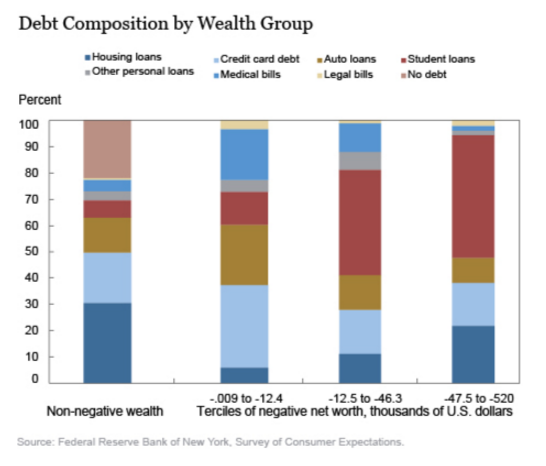

High levels of student debt are contributing to negative wealth -- when a household's debt is greater than its total assets -- and inequality, according to an analysis of household finance data by the Federal Reserve Bank of New York.

Student loans make up nearly half (47 percent) of the total debt of households with between $47,500 and $52,000 in negative wealth. For households with between $12,500 and $46,300 in negative wealth, college loans made up about 40 percent of total debt. In households with the smallest amounts of negative wealth, most debt was held in credit cards. The analysis is based on a 2015 special module on household finance from the Survey of Consumer Expectations, which includes data on respondents’ assets, debt and expectations from 1,300 respondents. About 15 percent of U.S. households have total wealth at or below zero, according to a blog post describing the findings.

Demographic data on negative wealth households show that they are younger, predominantly female, more likely to be minority, own homes at lower rates and have lower average annual incomes than households with nonnegative wealth. The authors of the analysis found that students or college graduates with negative wealth used debt to finance human capital investment and expected their financial status to be temporary as they attained higher incomes and paid off their loans. But households with negative wealth spend less and have more restricted credit.

Given the significance of student debt in explaining negative household wealth, the authors write, “it is likely that the steady growth in student debt and borrowing, combined with the very slow rate of student loan repayment we have documented elsewhere, has materially contributed and will continue to contribute to negative household wealth and wealth inequality.”

But Seton Hall University's Robert Kelchen, who studies issues related to student financial aid, said that conclusion may be going too far.

“It’s hard to draw that conclusion from this data,” said Kelchen, an assistant professor of higher education.

Kelchen said student loan debt is driving inequality among one group of students -- those who leave college without completing a degree. But he said many of the households with negative wealth include borrowers who took out student loan debt to pay for graduate school and professional degrees. That group will do well over all, Kelchen said.

The negative impact of student loan debt for those who leave college without a degree is gaining attention among higher ed policy makers. And recent research suggests that while student loan debt may have little effect on home ownership for those in high-earning jobs, it can have negative effects for those who do not finish a degree.

Another financial aid expert, Mark Kantrowitz, publisher and vice president for strategy at Cappex, said most students graduate college with an affordable amount of debt and it’s natural for them to have negative wealth immediately after graduation.

“The question is how does that progress over time,” he said. “Does that negative net worth become positive a decade after graduation or does it persist as negative?”

Kantrowitz said when people have to devote a substantial amount of their income to paying off student debt, it means they’re less capable of saving money to pay for retirement or put a down payment on a house. But he said the alternative scenario, where those individuals don’t take out loans, has to be considered as well.

“Would these individuals have been able to obtain a college education had they not borrowed?” he said. “And where would their net worth be if they hadn’t taken on this debt because they hadn’t gone to college?”