You have /5 articles left.

Sign up for a free account or log in.

iStock

Context is key for governing boards trying to exercise oversight of colleges and universities. It can also be surprisingly hard to come by, according to the American Council of Trustees and Alumni.

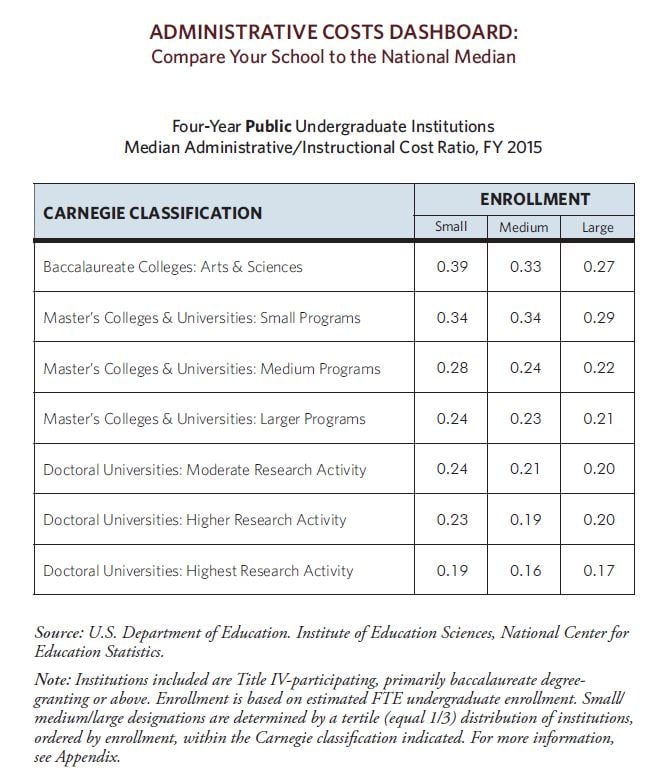

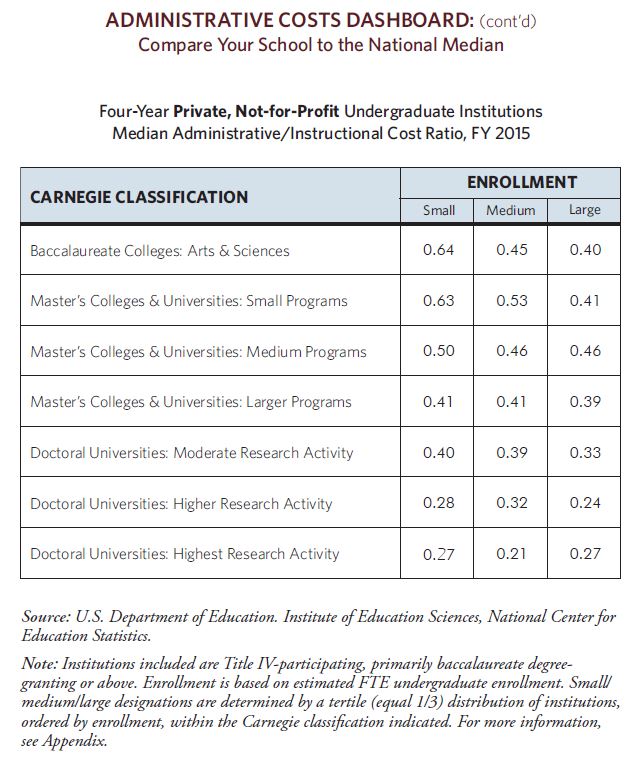

ACTA released new research today in an attempt to give trustees a financial benchmark for administrative spending and instructional costs. The group crunched 2015 data from more than 1,200 four-year nonprofit institutions to come up with median ratios of administrative spending to instructional spending for colleges and universities of various sizes and classifications.

The ratios come as many worry that administrative spending has risen faster than other types of spending at colleges and universities. ACTA wants them to be a tool for trustees trying to stop costs from rising. The group found that some types of small private nonprofit institutions spent a median of well over 50 cents on administration for every dollar they spent on instruction.

“People may be surprised, but it is the reality that not all boards receive the kind of financial information they need to make good, sound governance decisions,” said Michael Poliakoff, ACTA president.

“I hope this will be the springboard for a really good discussion,” he said. “Higher education governing boards typically have people who have been highly successful in the world of business and industry who understand profoundly the need for accurate metrics regularly delivered and carefully discussed.”

Skeptics and critics caution, however, that the ratio is not a perfect tool and can itself lack context. They warn that measuring administrative spending versus instructional spending is highly reliant on accounting practices that can be inexact -- or creative -- at some institutions. They also worried that trustees might be driven to move colleges and universities toward a median ratio that does not reflect the massive variations between different colleges and universities and the students they serve.

ACTA leaders say they attempted to be as conservative as possible when calculating the ratios, a process for which they used data from the National Center for Education Statistics Integrated Postsecondary Data System. The research ACTA released lists its definition of instructional cost as “expansive,” saying it includes what institutions report to NCES as expenses for instruction, functions that have direct bearing on institutions’ academic enterprise and academic support. Academic support is further defined as including expenditures for libraries, museums, galleries and academic deans. It does not cover department chairpersons, though.

Administrative costs are only defined as what institutions report to NCES as institutional support for the day-to-day operating support of an institution. That includes general administrative services, executive planning, legal operations, fiscal operations, public relations and development. But it does not include student services like student activities, career services and financial aid staff. Nor does it include auxiliary enterprises like parking, housing or food services. Expenses for operating hospitals are generally not included, either.

Athletics is not included in the calculation. Those expenses would typically fall under either student services or auxiliary expenses, according to ACTA. The report does not address either of those categories.

ACTA leaders believe that the current set of factors included in the ratio keeps it applicable to as many institutions as possible. But they want to look at other areas of spending, such as student services, in the future.

With those definitions explained, ACTA reports that the ratio of an institution’s spending on administration relative to instruction can show its budget priorities. Combined with other measures, it says, the ratio can provide warning when administrative operations are growing faster than core academic functions, which could drive up tuition and fees.

Generally, ACTA found that large institutions had a lower administrative-to-instructional cost ratio than small institutions.

For example, small private baccalaureate colleges posted a median ratio of 0.64, meaning they spent 64 cents on administrative costs for every $1 they spent on instructional costs. Large public doctoral universities classified as having the highest level of research activity had a median ratio of only 0.17.

There are some important caveats, however. The size categories are not the same for public institutions as they are for private ones. Generally, categories for public institutions covered larger colleges and universities than their counterparts for private institutions. For example, the category for large public doctoral universities with the highest research activity covered institutions with enrollment of 26,580 to 45,796. The same category for private institutions covered colleges and universities with enrollments spanning 9,221 to 27,004.

The benchmarks are not intended as a tool for comparison between different types of institutions, said Armand Alacbay, ACTA vice president of trustee and legislative affairs. They are supposed to be a way to encourage good board governance.

“The idea of having these categories is so that boards can have a back-of-the-envelope figure to compare similar institutions,” he said. “We’re not intending to have a cross-sector comparison here.”

Small institutions might also be expected to spend relatively higher amounts on administration than their larger counterparts. They have fewer students -- and consequently smaller instructional costs -- across which to spread spending that can’t be avoided, such as the cost of complying with government requirements.

Still, Poliakoff said, small institutions should take note of the findings.

“This is a wake-up call for small institutions, which are absolutely vital for American higher education,” he said. “A large segment of students need these kinds of small institutions, and they are the most vulnerable, which means they are going to have to think creatively, which means it is not OK to have a disparity between spending on administration and spending on instruction.”

ACTA gave four specific recommendations for trustees: that they be knowledgeable about administrative spending; that they establish a standard set of financial metrics to use when they are asked to approve a major expenditure; that they work to ensure data quality and consistency; and that they look for ways to consolidate administrative functions.

A wide-ranging call to cut administrative functions might not sit well with college and university leaders. Many administrators are likely to view the recommended ratio with unease.

Producing a ratio that applies accurately to the wide range of colleges and universities in American higher education is not easy, said Richard Kneedler, president emeritus of Franklin and Marshall College in Pennsylvania and former interim president at Rockford College in Illinois. Institutions of different sizes and types will need different spending levels, he said. So will institutions that serve different populations and institutions located in different areas.

“There is no system that’s going to account for a difference between an institution that has one building in the center of a town or a city and it’s not residential, and an institution that owns the top of a mountain somewhere in Tennessee and is responsible for 5,000 acres, has to have its own fire department and ambulance and police services and provide its own water and sewer,” Kneedler said. “Those are all administrative costs.”

Accounting practices can vary from institution to institution as well.

“You can’t do standard cost accounting in private higher education and have any certainty that from institution to institution you’re getting comparable numbers,” Kneedler said. “That really makes it troublesome to try to work across different institutions.”

Kneedler does not want to undercut the idea that there is value in benchmarking, he said. But he wanted to stress that the metrics sometimes make the story appear clearer than it actually is. Benchmarking is only a starting point from which to ask questions, he said.

Spending on administrative functions has generally outpaced spending in other areas, according to Steven Hurlburt, senior researcher at the American Institutes for Research and director of the Delta Cost Project.

Hurlburt outlined some notable differences between definitions ACTA used in calculating its ratio and those used in the Delta Cost Project. The ACTA definition of instruction differs from the Delta Cost Project’s education and related spending metric. ACTA’s inclusion of all expenses in the academic support category is wide-ranging.

“Academic support includes expenses of activities and services that support instruction, but also research and public service, which are definitely not related to instruction,” Hurlburt said in an email.

The Delta Cost Project calculation limits academic spending to its education-related portion.

Including academic support as a nonadministrative cost could also cause issues. Hurlburt gave the theoretical example of a college that moved to part-time contingent faculty but spent more on academic support administrators.

“The administration-to-instruction ratio would still be the same, but clearly less would be going to instruction and faculty,” he wrote.