You have /5 articles left.

Sign up for a free account or log in.

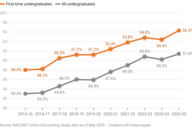

Nursing students have one of the highest rates of return on investment.

martinedoucet/Getty Images

Students pursuing a college degree generally have a sense of where their institution ranks in comparison to others, but not necessarily how their particular course of study measures up. Now they can find out. Using data from the latest College Scorecard, two new studies look much more granularly at how specific programs -- say, the bachelor’s degree in accounting at the University of Texas at Austin -- rate in helping recent graduates recoup their investments.

The two studies -- one from the center-left think tank Third Way and the other from the more conservative Texas Public Policy Foundation -- concur that while most college programs help graduates secure jobs that will allow them to repay their loans or recoup their costs within a few years, a sizable number do not. And knowing which is which, argue the authors of both, can not only help students make better-informed program choices but also guide policy makers in holding institutions accountable for failing programs.

“It used to be that you should go to the best college you could get into that you can afford,” said Andrew Gillen, senior policy analyst at the Texas Public Policy Foundation and the author of its study. “This program-level data helps lift that blindfold. If I know I’m interested in journalism, I can look up journalism programs at different schools and see what their graduates earn.”

By the same token, the data allow regulators to pinpoint high-debt, low-earning programs and implement sanctions or stricter oversight. “For excessive debt, the only participant that escapes unscathed is the institution,” Gillen said. “They got paid up front. But the student has debt they can’t afford, and the government can’t collect it.”

Some 43 million students presently owe nearly $1.6 trillion in federal student debt, according to government data. Such numbers warrant concern, said Martin Van Der Werf, the associate director of editorial and postsecondary policy at Georgetown University’s Center on Education and the Workforce. “I would like to see more regulatory crackdown particularly on programs that attract students who were promised a quick credential and then entry into a lucrative career,” he said. “And then they find out that that it was a waste of time -- the career really isn’t very lucrative, and the credential doesn’t have a lot of value. And it’s very costly. Those are the students who really need protection.”

The TPPF report examines student loan debt among recent graduates relative to their early-career earnings. It used College Scorecard data for more than 37,000 programs -- associate, bachelor’s, master’s, professional and doctoral -- that graduated more than 6.5 million students in the 2014-15 and 2015-16 academic years, measuring median debt against median annual earnings two years after graduation.

The study suggests two “accountability metrics” to help consumers distinguish between student loan debt that constitutes a “highly worthwhile educational investment” and that deemed a “financially hazardous malinvestment.”

The first measures median debt as a percentage of median earnings, recommending a four-tiered ranking system from “reward” (for programs with a debt-to-earnings ratio of less than 75 percent) to “sunset” (for those that exceed 125 percent). By those metrics, Gillen explained, 7.2 percent of all programs in the College Scorecard data set would be sanctioned, and another 6 percent would earn a “sunset” ranking, making them subject to increased regulatory oversight, financial aid counseling for currently enrolled students and a ban on enrolling new students using federal loans.

The second accountability option, Gillen said, is a revamped version of the gainful-employment rule, established by the Obama administration and then repealed by President Trump's Education Department, which aimed to hold low-performing vocational programs accountable for students with excessive debt. Gillen proposes applying the same formula as the defunct gainful-employment regime, which divides annual student loan payments by annual earnings, but using it for all programs and perhaps creating an alternative cutoff mechanism. That would put about 9 percent of the programs in the “failing” category.

Even good institutions can have programs with poor outcomes. The Wall Street Journal recently reported that graduates of Columbia University’s film school who took out federal student loans incurred a median debt of $181,000. Yet two years after receiving their master’s degrees, half of those borrowers were earning less than $30,000 a year. “When you’re doing institution-level accountability, Columbia is never going to fail,” says Gillen. “But when you do program-level, you can hold specific programs accountable.”

Examining data at the program level precludes assessing institutions with a single broad brush. “You can identify poor-performing programs at good institutions and exempt good-performing programs at poor institutions,” Gillen said. “One of the fields economists like to pick on is sociology. But when you actually look at the data, there are a ton of sociology programs that are doing great. If you ask me about any institution, I can find you a program that is doing great for students. And if you ask me about any program, I can find you a school with an excellent one.”

He favors deploying “carrots” as well as “sticks” in making institutions take responsibility for their offerings. “The entire approach to higher ed accountability so far has been that if you’re unacceptable at some metric, we’re going to punish you,” he says. “We do need sticks -- you need to sanction institutions -- but we should also have carrots: if you’re doing fantastic, maybe you can be exempt from regulatory oversight, or earn financial bonuses.”

Using the same data, the Third Way report evaluates which programs allow students to recoup the cost of their college education within five years of entering the workforce. Unlike TPPF’s report, it looks only at bachelor’s, associate and certificate programs and is concerned not with debt per se but with total cost.

Nearly two-thirds of all programs -- 64 percent -- allowed students to recoup their educational costs within 10 years of graduating, said Michael Itzkowitz, a senior fellow in higher education at Third Way and the author of the report. “By the same token, there are nearly 6,000 college programs -- about 16 percent of them -- that leave students with no return on investment, meaning that they’re earning even less than someone with no college experience whatsoever,” he said. “To put that in perspective, there were 353,000 students -- out of about 2.2 million in our data set -- who graduated from those programs. They’re leaving too many students underemployed or possibly underprepared to succeed in the 21st-century job market.”

Among those earning bachelor’s degrees, the Third Way report found that 100 percent of nursing and engineering students took five years or less to recoup their educational investments, compared to 44 percent in anthropology programs and 45 percent in religious studies.

Like Gillen, Itzkowitz is hopeful that these program-level data will have larger policy implications. “When it comes to student outcomes and taxpayer-funded programs, what we’re seeing is that there’s more agreement on both sides of the aisle,” he said. “So it’s essentially up to Congress to figure out a reasonable way to ensure that students are getting adequate preparation to succeed in the job market, and that taxpayer dollars are used efficiently.”

Not everyone agrees that earnings should be the primary measure of a program's value, even when taxpayer dollars are on the line. These studies look at how students fare early in their careers. And as Claude Pressnell Jr., president of the Tennessee Independent Colleges and Universities Association, has noted, sometimes the true worth of a college education doesn’t become clear for years or even decades. And there are plenty of ways to contribute to society besides repaying debts.

Van Der Werf believes the new studies are a valuable asset but that they need to go further to really serve the consumer. “They’re important to higher ed researchers, but they won’t make any difference to the public until you actually name the programs,” he said. “Where you go to school and what degree you pursue is not always a rational economic choice. But I think it needs to be more and more so. And these kinds of tools, hopefully, will allow people to make a little bit wiser investment.”