You have /5 articles left.

Sign up for a free account or log in.

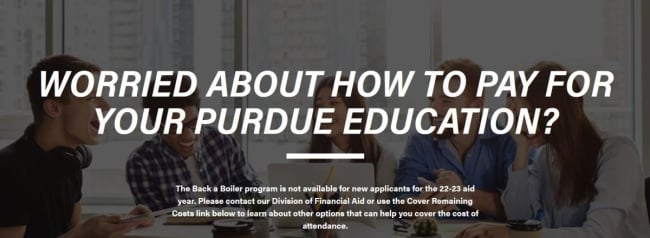

Purdue paused its income-share agreement earlier this month, announcing the move in a banner on its website.

Purdue University

Purdue University has paused new enrollments in its income-share agreement program, a financing mechanism both praised as a bold experiment to make college more accessible and criticized as a predatory scheme that traps students in dodgy and expensive contracts.

Known as Back a Boiler, the program was quietly paused earlier this month, with a message posted on Purdue’s website around the same time that President Mitch Daniels announced his forthcoming retirement and a successor was selected through a secretive search process.

Purdue officials say suspending Back a Boiler is a technical matter, citing a change from one vendor to a different one that doesn’t originate new income-share agreements but will continue to service existing ones. Critics, however, believe that pausing new enrollments marks the death of the Back a Boiler program.

Other higher ed observers wonder what the pause signals for the future of such agreements.

The Back a Boiler Experiment

Launched in 2016, Back a Boiler was hailed as a revolutionary new way to pay for college. The program, which Purdue has called an alternative to Parent PLUS loans and private student loans, was initially available only to juniors and seniors, then expanded to include sophomores.

Exactly how income-share agreements, or ISAs, are structured depends on a variety of factors, including a student’s chosen major and their projected earning potential. Generally, borrowers agree to pay back a portion of their projected income over a certain number of years.

ISA providers have long argued that their product is not a loan but an altogether different type of agreement. However, the Department of Education sank that notion in March when it issued a clarification stating that ISAs are indeed private student loans. (A sample contract on Purdue’s website currently states that the Back a Boiler program “is not a loan.”)

Purdue’s website describes its income-share agreement as “an innovative new way to help make school more affordable for Purdue students” and “a potentially less expensive option” than traditional student loans, given that interest does not accrue on the amount borrowed via an ISA.

Since 2016, Purdue has signed more than 1,900 income-share agreements with students, disbursing $21 million backed by the Purdue Research Foundation, which solicits investors—including hedge funds—to provide money for Back a Boiler.

According to Purdue, the pause comes as a result of switching its ISA servicing operations from Vemo Education to Launch Servicing, which does not provide support for originating ISAs.

“After Vemo’s departure, [the Purdue Research Foundation] was not able to timely identify a suitable successor meeting PRF’s high standards for ISA origination activities in the coming academic year. PRF therefore decided to pause new ISA originations under Back a Boiler for the time being, while continuing to service the ISAs already outstanding under the program,” Purdue spokesperson Tom Doty told Inside Higher Ed via email. “To be clear, nothing about this pause affects those existing ISAs. PRF’s hope and expectation is that, as policymakers continue to provide greater regulatory certainty around ISAs and as additional market participants enter this space, more potential vendors will be available to support programs like Back a Boiler.”

Doty added that Purdue is not actively seeking a servicer to originate new ISAs because there isn’t enough time before the next academic year begins.

But critics—who have complained to regulatory agencies that Back a Boiler is illegal and predatory—are skeptical of Purdue’s claims.

“They’ve got their press statement about how they moved from Vemo and now Launch doesn’t do origination. Bullshit. If they wanted to find an origination partner they could,” said Ben Kaufman, director of research and investigations at the Student Borrower Protection Center. “So, the program failed. You mean to tell me that this was an organic movement away when, in fact, they announced it at 4:30 p.m. on a Friday, on the day that Mitch Daniels resigned?”

Long critical of Purdue’s ISA program, the Student Borrower Protection Center sent a letter to the Department of Education and the Consumer Financial Protection Bureau in March, arguing that the university violated the Higher Education Act by “co-branding private loan products with student lenders,” among other issues, and calling for an investigation.

Purdue described the allegations made by the Student Borrower Protection Center as false and said it has not been contacted by the Department of Education or the Consumer Financial Protection Bureau.

The Department of Education did not answer questions about Purdue’s ISA program, but a response from the CFPB struck a sharp tone on questionable student loan products.

“There is a lengthy and troubling history of exotic financial products targeting students. The CFPB has taken action to address predatory student loan products in the past, and will continue to hold firms accountable for noncompliance with federal consumer financial law,” the CFPB press office said in an email to Inside Higher Ed.

Recent Purdue graduates have also criticized the program, noting that their participation in Back a Boiler left them with massive debt loads and inept servicers who mishandled their loan payments.

The Opaque Future of ISAs

When Purdue jumped into the ISA marketplace some six years ago it was—and arguably still is—the biggest name to do so. The fact that it has now hit pause has prompted some higher ed observers to question the marketplace potential for such agreements.

Justin Draeger, president and CEO of the National Association of Student Financial Aid Administrators, noted that despite the attention ISA programs receive, there are relatively few nationwide. Though many colleges have expressed interest, few have entered the marketplace.

“For most schools, I think they looked at income-share agreements as experimental,” Draeger said, adding that many questions remain about the efficacy of ISAs—including student outcomes, such as how graduates are navigating repayment and how low-income borrowers fare in such arrangements.

Ethan Pollack, director of the Financing the Future initiative at the nonprofit Jobs for the Future, said by email there is “no comprehensive data on the ISA market, so we don’t know exactly how big the ISA market is or how many students it serves.” He added that ISAs are “more common for vocational training programs than for traditional higher education degree programs.”

Beth Akers, an economist and senior fellow at the center-right think tank the American Enterprise Institute, noted that Purdue was an early adopter of ISAs, which prompted “very quick growth” in the marketplace, though she said colleges are still wary of adopting such financing mechanisms.

One reason for the limited growth of ISAs, she added, is the “open hostility” of lawmakers.

To Akers’s point, some prominent politicians, including Massachusetts senator Elizabeth Warren, have taken aim at income-share agreements. Warren, along with Democratic representatives Ayanna Pressley of Massachusetts and Katie Porter of California, wrote a letter in 2019 to then education secretary Betsy DeVos questioning a Trump administration plan to experiment with ISAs.

“At a time when student debt stands at more than $1.5 trillion, it is deeply disturbing to see a Department official boosting novel forms of student debt instead of trying to stem the tide of indebtedness—and even more disturbing to hear the official propose using federal taxpayer dollars to do so,” they wrote.

Akers—who has written about the possibility of replacing the federal student loan system with income-share agreements—suggested that the Department of Education under the Biden administration has also thwarted growth in the ISA marketplace by showing hostility toward colleges considering such moves.

“The tone from the Department of Education in their communication on this issue implies some hostility towards the model. And I think even though there are benefits to an institution, to students, that creates a lot of liability for an institution and a lot of headaches,” Akers said.

ISA critics, such as Kaufman at the Student Borrower Protection Center, argue that income-share agreements are often confusing to borrowers and offer little transparency.

“In case after case, ISAs proved to be much more complex than people understand, to be much more expensive than they understand, to involve much harsher terms than people think and to not actually have a lot of the downside protections that people think they will. Instead, they very often [are] a linchpin in the business model of fraudulent and scammy boot camps,” Kaufman said.

Observers on all sides of the issue are concerned about the lack of clear guidelines.

“Perhaps the biggest challenge is that it’s entirely unclear how ISA providers should comply with existing consumer credit regulations,” Pollack said in an email. “The government needs to be clear about how it expects ISA providers to comply with the law, and until it does that, ISA providers will continue to operate in regulatory uncertainty.”

Regardless of what the future holds for ISAs, experts suggest there is an appetite for alternative college financing mechanisms, in part because the current financial aid system is flawed. And when consumers have a bad experience, they’ll ultimately look elsewhere for better products.

“The entire reason income-share agreements even had a wedge into the student loan marketplace is because of the dissatisfaction by students, parents and schools, for that matter, with our current federal student loan system. I’m not one of the people that sees ISAs as evil. I don’t necessarily see them as good. I see them as a reality and a market-based response to the general malaise and dissatisfaction people feel with our current education financing system,” Draeger said.